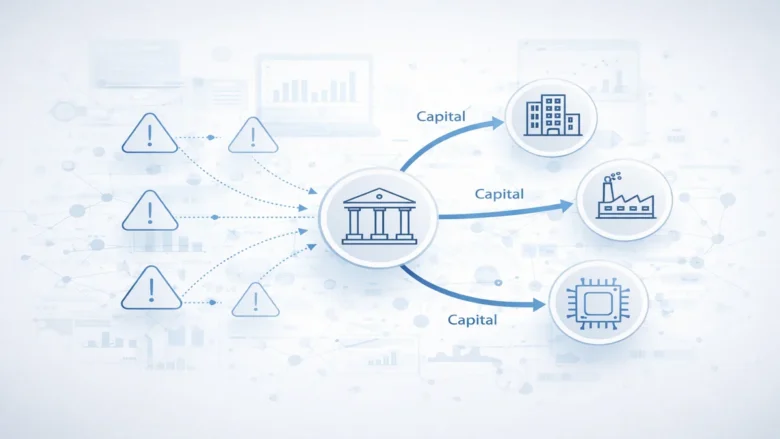

In today’s global financial system, capital moves through complex regulatory frameworks, interconnected funding sources, and trading platforms that shape how risk is managed and shared. Investment decisions are influenced not only by expected returns but also by rules for clearing trades, standards for reporting, margin requirements, and systems for monitoring financial institutions. Banks, institutional investors, …

Over the past three decades, supervisory authorities, rating agencies, and capital markets have transformed how extreme-event risks are managed. Increasing climate instability, seismic concentrations in urban areas, and highly interconnected supply chains have forced insurers and reinsurers to rethink how balance sheets handle low-frequency, high-severity events. Regulatory frameworks increasingly integrate stress testing calibrated to extreme …

Consumer lending can feel complicated. From loans for cars and homes to personal lines of credit, the process involves rules, risk assessments, and careful planning. When I first started learning about how lending works, terms like “underwriting,” “risk segmentation,” and “macroprudential oversight” seemed overwhelming. But over time, I realized that at its core, lending is …

Credit markets are the backbone of modern finance. Banks, investors, and capital market participants rely on the certainty that borrowers will meet their repayment obligations. When that certainty falters, financing costs rise, liquidity tightens, and capital allocation becomes more selective. To mitigate these pressures, financial systems have developed layered credit protection and default risk mechanisms. …

Retail finance operates at massive scale. Payment cards, digital wallets, consumer lending platforms, and online banking interfaces process millions of transactions daily. While this transaction volume increases efficiency, it also exposes institutions to significant fraud risk. Regulatory authorities treat fraud not only as a criminal concern but also as an operational and conduct risk that …

Governments, central banks, and large institutions often discuss financial stability. However, the foundation of a resilient financial system actually begins much closer to home—with households, small businesses, and nonprofit organizations. In today’s evolving economic environment, these entities are increasingly encouraged by policymakers and regulators to maintain accessible liquidity buffers that can absorb unexpected shocks. Emergency …

Property insurance markets operate in an increasingly complex environment shaped by natural disasters, urban development, and rising construction costs. These factors significantly influence the volume and complexity of insurance claims filed by policyholders. After major disasters such as hurricanes, floods, or wildfires, insurers may receive thousands of claims within a short period. At the same …

Life insurance products are designed to manage financial obligations that may extend across several decades. Unlike many other financial contracts, life insurance policies often involve long-term liabilities that must remain financially sustainable over extended periods. For this reason, premium pricing in life insurance is not determined solely by actuarial calculations. Instead, it reflects a combination …

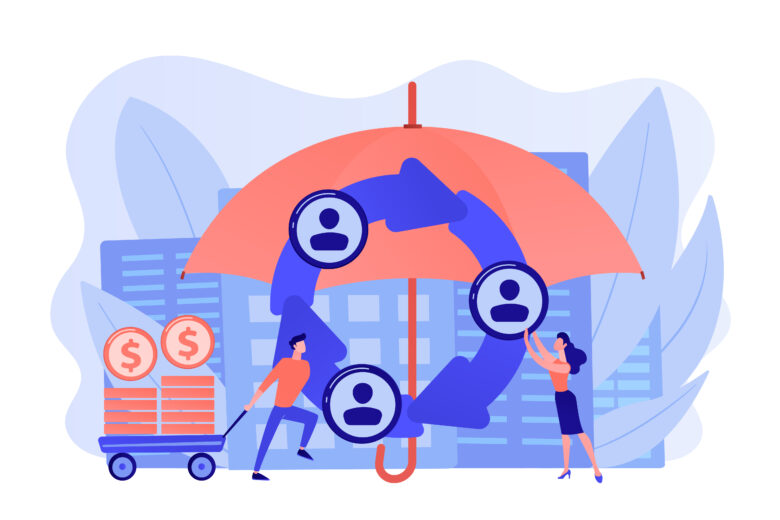

Insurance markets operate through a continuous circulation of capital. Premium inflows, reserve allocations, administrative buffers, and reinsurance recoverables move through regulatory and institutional frameworks designed to distribute risk across time and between participants. At the center of this system lies risk pooling. Rather than functioning as simple collections of claims, risk pools operate as structured …