One ignored email. One small overdraft. One catastrophic cascade. How a single $12 fee spiraled into an $847 lesson I will never forget. I still remember the exact moment I realized something was wrong. It was a Tuesday morning, 7:42 AM, and I was standing in line at a coffee shop. My card got declined. For a $4.50 latte. I had $847 in my account — or at least, I thought I did.

The barista was nice about it. She had seen it before. I muttered something about a glitch, paid with cash, and walked out feeling embarrassed but not alarmed. Banks do not make mistakes, I told myself. There must be a simple explanation. There was an explanation. It was not simple. And it was entirely my fault.

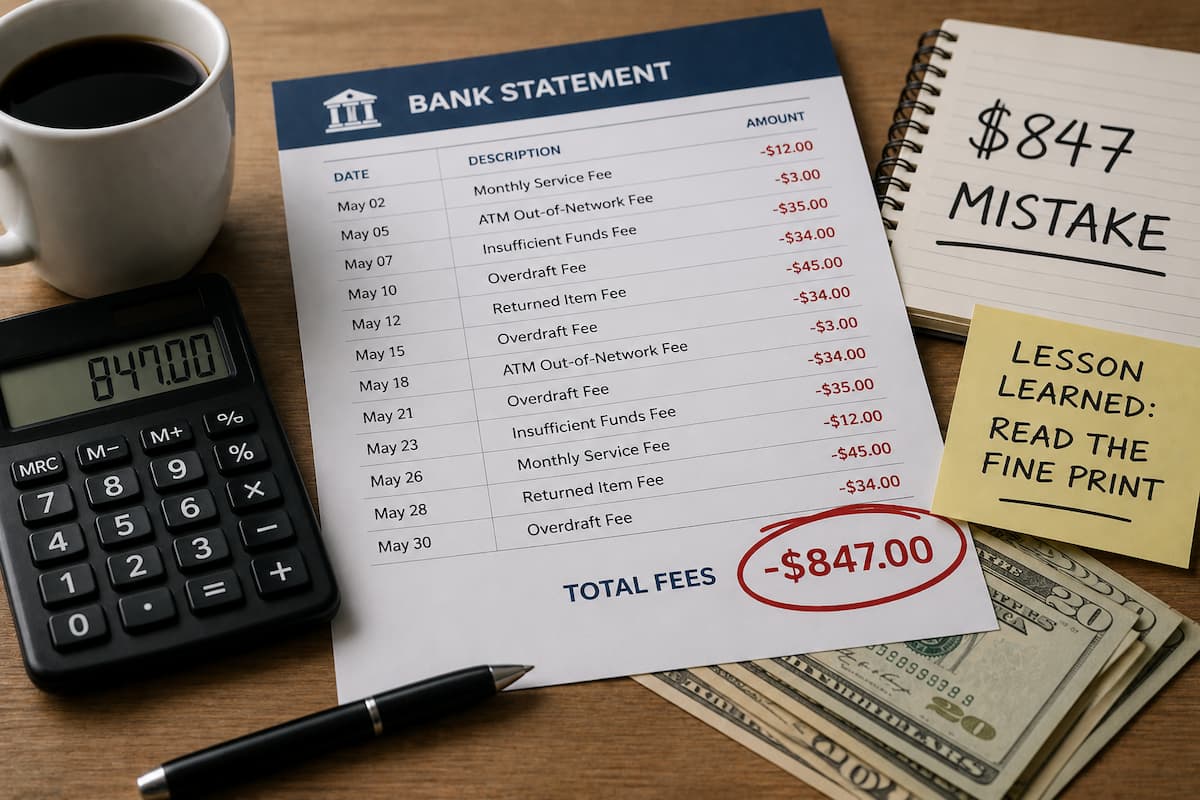

How $12 Became $847

The cascade started three weeks earlier, on a Friday I barely remembered. I had written a check for my rent — $1,200 — and dropped it in the mail. The check cleared on Monday. What I did not know was that my paycheck, which usually arrived Tuesday, had been delayed by a holiday. For 24 hours, my account was overdrawn by $89.

That $89 overdraft triggered a $35 overdraft fee. Fair enough, I suppose. I had messed up the timing. But here is what I did not understand: the bank processed my transactions in an order that maximized fees, not in the order they occurred.

I assumed the bank processed transactions chronologically — first in, first out. Instead, they processed the largest transaction first (my rent check), then the smaller ones. This meant my account went deeply negative immediately, and every subsequent small transaction — a $12 lunch, a $8 parking fee, a $4 coffee — each triggered its own $35 overdraft fee. Five transactions. Five fees. $175 in a single day.

But that was just the beginning. Because my account was now negative, my automatic savings transfer — $50 per month — failed. The bank charged a $25 returned transfer fee. My gym membership, also automatic, failed. Another $25 fee. A subscription I had forgotten about tried to charge. Failed. Another fee.

By the time I checked my balance three days later, I had accumulated $312 in overdraft and returned payment fees. I called the bank. The representative was polite but firm. “These fees are clearly disclosed in your account agreement.” I had signed it. I had not read it. That was my problem, not theirs.

47 days × $7 = $329. Added to the $312 in initial fees. Total: $641. Then, because my account had been negative for more than 30 days, the bank closed my savings account — the one with my emergency fund — and transferred the balance to cover the checking account deficit. They charged a $50 account closure fee. Then a $56 fee for “excessive negative balance duration.” Then a $100 fee for “account rehabilitation.”

Total damage: $847. For a single missed paycheck timing. For not reading the fee schedule. For not checking my account for 47 days. For assuming my bank would warn me before destroying my finances.

• 5 overdraft fees @ $35 each: $175

• 3 returned payment fees @ $25 each: $75

• 47 daily maintenance fees @ $7 each: $329

• Savings account closure fee: $50

• Negative balance duration fee: $56

• Account rehabilitation fee: $100

• Grand Total: $847

What I Learned About How Banks Actually Work

Before this experience, I thought of banks as neutral custodians. They held my money, processed my transactions, and charged modest fees for the service. After this experience, I understood that banks are businesses. Their business model includes fee income. And fee income is most profitable when customers are least aware of it.

Here is what I learned, in the order that shocked me most:

Transaction Ordering Is Not Chronological

Banks can process transactions in any order they choose. Most choose largest-first, which maximizes overdraft fees. A $1,200 rent check followed by five small purchases creates six overdraft opportunities. The same transactions processed smallest-first might create only one. The bank chooses the method that generates more revenue. This is legal. This is disclosed. Most people never read the disclosure.

Overdraft “Protection” Is Often a Trap

I had “overdraft protection” enabled. It sounded helpful. In reality, it meant the bank would cover overdrafts — for a fee — rather than declining transactions. Without overdraft protection, my card would have been declined at the coffee shop. Embarrassing, but cheap. With overdraft protection, the transaction went through, and I paid $35 for the privilege of buying a $4 latte I could not afford.

Maintenance Fees Compound Silently

The $7 daily fee was the cruelest part. It was small enough to ignore, large enough to destroy. $7 feels like nothing. $7 for 47 days feels like theft. And because it was automatic, there was no transaction to trigger my awareness. No alert. No email. Just a quietly growing deficit that I did not see because I was not looking.

Account Closure Does Not Stop the Bleeding

I assumed closing the account would end the fees. It did not. The bank continued charging “rehabilitation” fees on the closed account until the balance was paid. Closing the account actually added fees rather than stopping them. The only way out was to pay the full negative balance plus all accumulated charges.

Banks Are Not Required to Warn You

This was the hardest lesson. I expected a phone call, an email, a letter — some human intervention before $847 disappeared. There was none. The bank sent statements. I did not open them. The bank sent emails. I filtered them as spam. The bank fulfilled its legal obligation to disclose. I fulfilled my obligation to ignore it. The responsibility was mine.

What I Changed After the $847 Lesson

The experience was expensive, humiliating, and entirely preventable. Here is the system I built afterward, piece by piece, to ensure it never happened again:

I Read the Fee Schedule

Not skimmed. Read. Every page. Every condition. Every trigger. I now know exactly what my bank charges and when. I know the order of transaction processing. I know the overdraft policy. I know the daily maintenance fees. I know the account closure fees. Knowledge is not power in this context — knowledge is armor.

I Turned Off Overdraft Protection

I called the bank and opted out. Now, if my account lacks sufficient funds, the transaction is declined. Yes, it is embarrassing at the register. Yes, it requires better planning. But a moment of embarrassment costs $0. A moment of overdraft “convenience” costs $35. The math is simple.

I Set Up Balance Alerts

Every bank offers them. Most people do not use them. I set three alerts: one when my balance drops below $200, one when a transaction over $100 occurs, and one when my account goes negative. The $200 alert gives me time to transfer money. The $100 alert catches unusual activity. The negative alert is my emergency brake.

I Switched to a Fee-Transparent Bank

Not all banks are equal. After my experience, I researched alternatives. I found a credit union with no overdraft fees, no daily maintenance fees, no account closure fees, and chronological transaction processing. The interest rate was slightly lower. The peace of mind was infinitely higher. I switched within a month.

I Check My Balance Every Morning

Not obsessively. Not anxiously. Just a 30-second glance while my coffee brews. I look at the balance, scan the recent transactions, and confirm nothing looks wrong. This habit takes less time than brushing my teeth and has saved me from at least three potential issues in the past year — a duplicate charge, a subscription I forgot to cancel, and a fraudulent small test transaction.

I Keep a Micro Buffer

I now maintain $300 in my checking account that I treat as $0. It is not part of my budget. It is not available for spending. It is a shock absorber for timing mismatches — a delayed deposit, an early automatic withdrawal, a check that clears faster than expected. That $300 has prevented at least two overdraft situations since I started the practice.

The Questions I Now Ask Every Bank

Before opening any account, I ask five questions. The answers determine whether I proceed:

- How do you process transactions? Largest-first? Chronological? Batch? The answer reveals fee risk.

- What is your overdraft policy? Decline? Cover with fee? Transfer from savings? The best answer is decline or free savings transfer.

- What daily fees apply to negative balances? Any answer other than “none” is a red flag.

- What alerts can I set? Limited alert options mean limited awareness. I want granular control.

- What are your account closure fees? High closure fees trap you in a bad relationship. Low or no closure fees respect your freedom to leave.

No bank has perfect answers to all five. But the conversation itself is revealing. Banks that are transparent about fees tend to have lower fees. Banks that deflect, obfuscate, or redirect tend to have fee structures designed to catch you unaware.

What I Would Tell Myself Before It Happened

If I could send a message to myself three months before the $847 mistake, it would be short:

Your bank is not your friend. It is a business that makes money from your inattention. Read the fee schedule. Check your balance. Turn off overdraft protection. Set alerts. Assume that every convenience feature has a cost, and every cost compounds when you are not looking. The $4 latte is not the problem. The $35 fee for the $4 latte is the problem. And the $7 daily fee for the $35 fee for the $4 latte is the catastrophe.

Prevention is boring. Recovery is expensive. Choose boring.